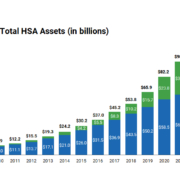

The IRS has recently released the contribution limits for Health Savings Accounts (HSAs) for 2025. In 2024 we saw a significant increase, mainly in response to continued pressures from inflation. In the upcoming year, we will see another adjustment upwards, yet smaller than the 2024 increases.

For 2025, individuals with self-only coverage can contribute up to $4,300 to their HSAs, up from $4,150 in 2024. Family plans can contribute up to $8,550, up from $8,300 in 2024. This change reflects a steady acknowledgment of the need for greater financial flexibility in managing health expenses.

The IRS hasn’t released the 2025 catch-up contribution yet for those age 55 and older. It is currently set at $1,000 for 2024, unchanged from 2023.

According to Fidelity Investments’ 2023 Retiree Health Care Cost Estimate, a 65-year-old retiring this year can expect to spend an average of $157,500, or $315,000 per couple, in health care and medical expenses throughout retirement. Understanding how to save and invest with an HSA plan is key to helping you plan for future expected and unexpected medical expenses.

If you are in an HSA and have questions about how to get the most out of the plan, CalCPA Health can help answer your questions. Approximately 45% of CalCPA Health medical subscribers are enrolled in a Health Savings Account. Education is key and CalCPA Health is here to help – whether you are in one of our HSA plans or not. We are a resource for you – feel free to ask questions by emailing info@calcpahealth.com.

Exciting news: Chuck Gielow received the CalCPA Distinguished Service Award! Here at CalCPA Health, CalCPA member firms have access to quality health insurance and benefit products. Chuck is one of CalCPA Health’s first Board members and was the Board Chair from 2013-2018. He is a huge advocate for CalCPA members and deserves this special recognition!

Exciting news: Chuck Gielow received the CalCPA Distinguished Service Award! Here at CalCPA Health, CalCPA member firms have access to quality health insurance and benefit products. Chuck is one of CalCPA Health’s first Board members and was the Board Chair from 2013-2018. He is a huge advocate for CalCPA members and deserves this special recognition!

The new California Law, SB 1375, was signed by Governor Brown on September 22, 2018 and will affect many small firm’s group health insurance. SB 1375 changes the Health Insurance Code to reclassify certain small employer groups as individuals. The affected firms will have to obtain individual health insurance in 2019, rather than the small employer group plans they currently have. Individual health insurance is typically more expensive with less provider network and benefit plan choices than small group plan offerings.

The new California Law, SB 1375, was signed by Governor Brown on September 22, 2018 and will affect many small firm’s group health insurance. SB 1375 changes the Health Insurance Code to reclassify certain small employer groups as individuals. The affected firms will have to obtain individual health insurance in 2019, rather than the small employer group plans they currently have. Individual health insurance is typically more expensive with less provider network and benefit plan choices than small group plan offerings.