2023 Health Savings Accounts Limits Are Released By The IRS

The IRS has released the contribution limits for Health Savings Accounts (HSA) for 2023 and the numbers are significantly higher than in prior years, as you can see from the chart below. Knowing these numbers will help employers prepare for open enrollment and think about their contribution levels as well as help employees understand the benefits of contributing to their HSAs.

| Tax Year | Individual Coverage Limit | Family Coverage Limit |

| 2023 | $3,850 | $7,750 |

| 2022 | $3,650 | $7,300 |

| 2021 | $3,600 | $7,200 |

| At age 55, members are allowed to contribute and additional $1,000 | ||

What is a HSA? It is a tax-advantaged account, paired with a high-deductible health insurance plan (HDHP), that allows you to save pre-tax dollars for future qualified medical expenses. You can invest the funds in the HSA account tax-free and grow your savings. You own the account, it travels with you if you change jobs, change your health plan, or retire.

To qualify for a HSA you must be enrolled in a qualified high-deductible health plan and meet the following criteria:

To qualify for a HSA you must be enrolled in a qualified high-deductible health plan and meet the following criteria:

- Must be a U.S. taxpayer

- May not be covered by another non-qualified plan (including Medicare coverage)

- May not be claimed as a dependent on someone else’s tax return

- May not be receiving Veterans Affairs benefits within the past three months

Qualified high-deductible health plans typically offer lower premiums, allowing both the employer and employee reduced costs. Employees and employers can put the money they would normally would have spent on premiums, into the HSA and building account balance for future medical expenses.

The investment side of HSAs is often overlooked. HSAs allow for long-term savings, similar to a 401K account. The difference however is that the HSA allows you to take tax-free distributions for qualified medical expenses. Withdrawals from a HSA, contributions and investment gains, if used for medical expenses are not taxed (federal). And if non-medical distributions are taken in retirement, it is taxed similarly to an IRA/401k.

According to a recent report, the average retired couple age 65 in 2022 may need approximately $315,000 saved (after tax) to cover health care expenses in retirement.* Knowing the facts will help people not only save future spending dollars in their HSA account, but also help them learn how to comparison shop for healthcare procedures or providers.

Currently, almost half of the CalCPA Health membership is enrolled in HSA’s. Education is key to understanding just how valuable it is to have a HSA and how to make it work for you. CalCPA Health can help answers you may have about HSAs – contact us whether you are enrolled in one of our medical plans or not. We are here to help the CalCPA community – info@calcpahealth.com.

* https://www.fidelity.com/viewpoints/personal-finance/plan-for-rising-health-care-costs

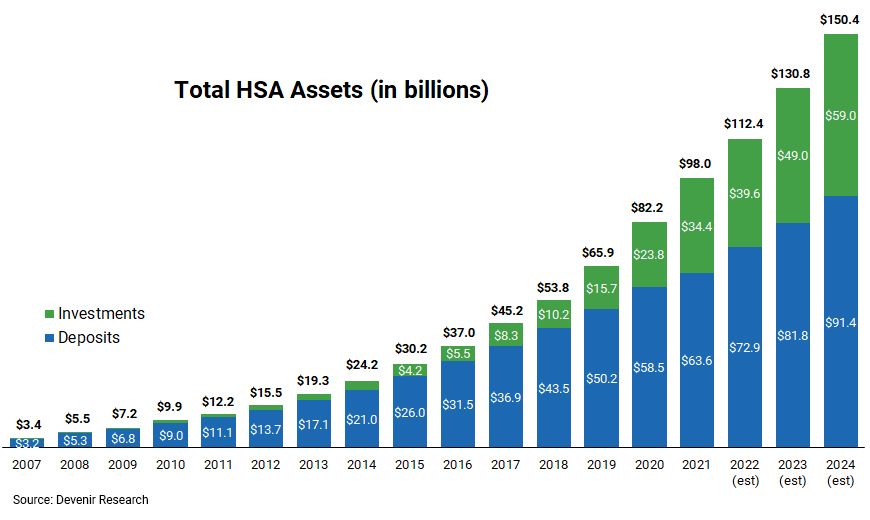

Chart Source: Devenir Research https://www.devenir.com/research/2021-year-end-devenir-hsa-research-report/

Leave a Reply

Want to join the discussion?Feel free to contribute!